(click image to enlarge)

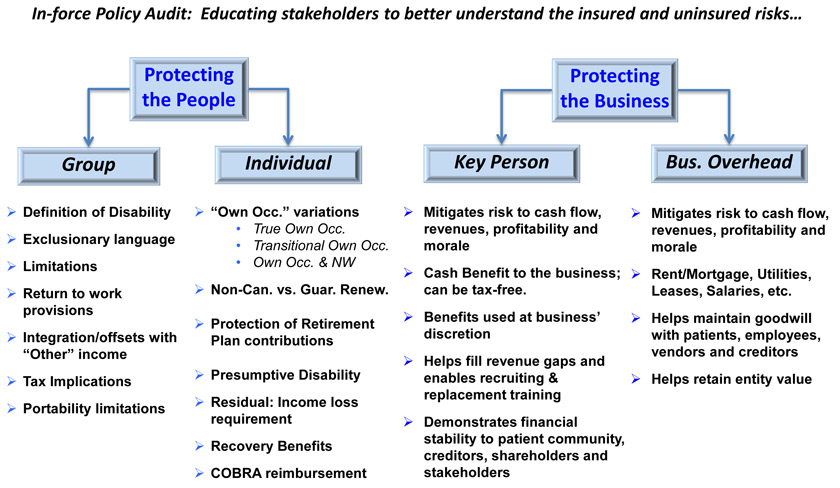

The focus of our disability income solutions is two fold: 1) Protecting individuals’ income and 2) Protecting the success of the business/entity. There are a myriad of products and solutions available in the marketplace…which ones fit depend on the specific situation and the goals of the policy owner:

Protecting the Individual

- Individual Disability Insurance (IDI)

- Retirement Plan Protection

Protecting the Business:

- Business Overhead Expense (BOE)

- Key Employee Protection

Understanding the contractual language within a disability insurance policy is critical as not all policies are created equal. Many understand that an “Own Occupation” definition of disability is paramount. However, what many don’t realize is that three variations of the “Own Occupation” definition exist – two of which are not really true “Own Occupation”. Simply put, unless you understand the fine print, it can make the difference between collecting and not collecting.

We take the time to understand and explain how your current policy works. We will outline options for improving the policy, if necessary, so that you are more in control at time of claim.

For those seeking new coverage, we craft programs designed to meet your needs and budgets through listening and understanding to your concerns and goals. A variety of leading carriers will compete assuring the most optimal solution.